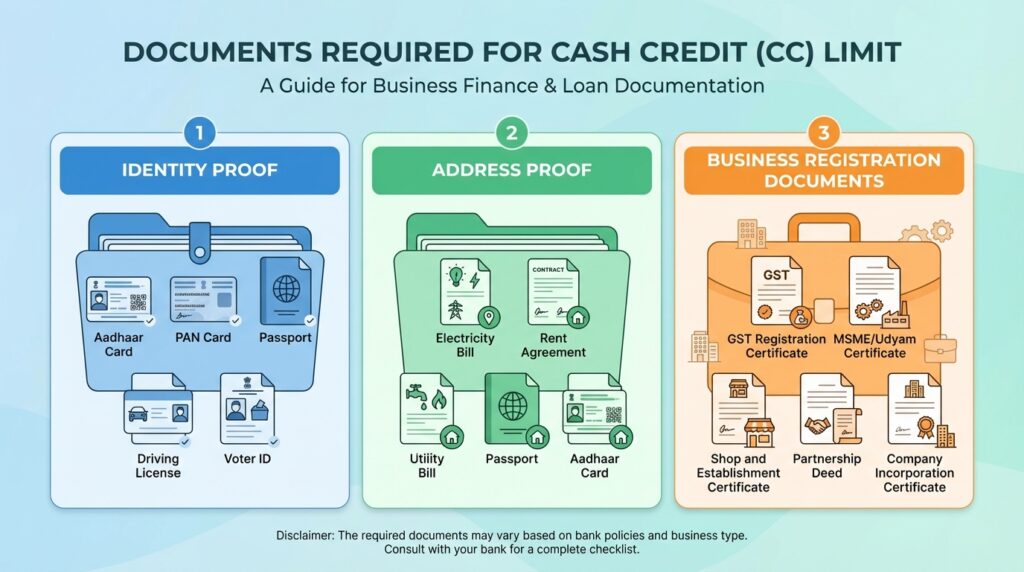

CC लिमिट के लिए कौन से दस्तावेज चाहिए | Business CC Limit Documents

अगर आप अपने business के लिए Cash Credit (CC) Limit लेना चाहते हैं, तो सबसे पहले यह जानना जरूरी है कि बैंक CC लिमिट के लिए कौन से दस्तावेज चाहिए। कई बार business owners केवल process जानते हैं, लेकिन सही documents की जानकारी न होने के कारण उनकी application delay हो जाती है या reject भी हो सकती है।

CC Limit खासतौर पर working capital की जरूरतों को पूरा करने के लिए दी जाती है, जिससे businesses अपने daily expenses, inventory purchase और operational costs आसानी से manage कर सकें। लेकिन इस facility को approve करने से पहले bank applicant की identity, business details और financial stability को verify करता है।

इस article में हम विस्तार से समझेंगे कि CC लिमिट के लिए कौन से दस्तावेज चाहिए, bank किन factors को check करता है और application process को smooth बनाने के लिए आपको किन बातों का ध्यान रखना चाहिए।

CC Limit क्या होती है?

Cash Credit Limit (CC Limit) एक प्रकार की working capital loan facility होती है जो बैंक businesses को उनके रोज़मर्रा के खर्चों और operational जरूरतों को पूरा करने के लिए देता है। यह सुविधा खासतौर पर उन businesses के लिए होती है जिन्हें अपने व्यापार को चलाने के लिए समय-समय पर पैसे की जरूरत पड़ती है।

CC Limit में बैंक एक maximum limit तय करता है, और borrower उसी limit के अंदर जरूरत के अनुसार पैसा निकाल सकता है। इसमें सबसे बड़ी खासियत यह है कि interest केवल उसी amount पर लगता है जो आपने वास्तव में इस्तेमाल किया है, पूरी limit पर नहीं।

उदाहरण के लिए, अगर किसी business को बैंक ने ₹10 लाख की CC Limit दी है और वह केवल ₹4 लाख ही इस्तेमाल करता है, तो उसे interest भी केवल ₹4 लाख पर ही देना होगा। यह facility businesses को inventory खरीदने, suppliers को payment करने और daily business expenses manage करने में काफी मदद करती है। इसलिए CC Limit को business financing का एक महत्वपूर्ण और flexible विकल्प माना जाता है।

CC Limit के लिए कौन से दस्तावेज चाहिए?

1. पहचान प्रमाण (Identity Proof)

जब आप CC Limit के लिए आवेदन करते हैं, तो बैंक सबसे पहले आपकी पहचान (Identity) को verify करता है। इससे बैंक यह सुनिश्चित करता है कि loan के लिए apply करने वाला व्यक्ति वास्तविक है और उसकी personal details सही हैं। Identity proof के रूप में आमतौर पर सरकार द्वारा जारी किए गए documents स्वीकार किए जाते हैं।

Common Identity Proof Documents:

- Aadhaar Card

- PAN Card

- Passport

- Driving License

- Voter ID Card

इन documents की मदद से बैंक applicant की personal identity और KYC (Know Your Customer) process पूरी करता है।

2. पता प्रमाण (Address Proof)

CC Limit देने से पहले बैंक applicant का residential या business address verify करता है। इससे बैंक को यह पता चलता है कि borrower का स्थायी पता क्या है और वह कहाँ रहता या business करता है। Address proof के रूप में ऐसे documents मांगे जाते हैं जिनमें applicant का पूरा और सही address clearly लिखा हुआ हो।

Common Address Proof Documents:

- Aadhaar Card

- Electricity Bill

- Rent Agreement

- Passport

- Utility Bills

Bank आमतौर पर recent utility bills (2–3 महीने के अंदर) मांगता है ताकि current address verify किया जा सके।

3. Business Registration Documents

अगर आप business के नाम पर CC Limit लेना चाहते हैं, तो बैंक यह देखना चाहता है कि आपका business कानूनी रूप से registered और active है। इसके लिए आपको business registration से जुड़े documents जमा करने पड़ते हैं। इन documents से बैंक को business की legal identity, structure और operational status के बारे में जानकारी मिलती है।

Common Business Registration Documents:

- GST Registration Certificate: अगर आपका business GST के तहत registered है, तो GST certificate bank को यह दिखाता है कि आपका business officially registered है और tax system में active है।

- Shop and Establishment Certificate: कई राज्यों में business establishments को local authority के साथ register करना होता है। यह certificate business location और operation का proof होता है।

- MSME Registration (Udyam Registration): अगर आपका business micro, small या medium enterprise category में आता है, तो MSME registration certificate bank के लिए एक strong supporting document होता है।

- Partnership Deed: अगर business partnership firm है, तो partnership deed यह बताता है कि business के partners कौन हैं और उनकी responsibilities क्या हैं।

- Company Incorporation Certificate: अगर business private limited या limited company है, तो Ministry of Corporate Affairs (MCA) द्वारा जारी incorporation certificate business की legal identity को साबित करता है।

इन documents के आधार पर bank यह समझता है कि business legally established है, कितने समय से चल रहा है और उसका ownership structure क्या है।

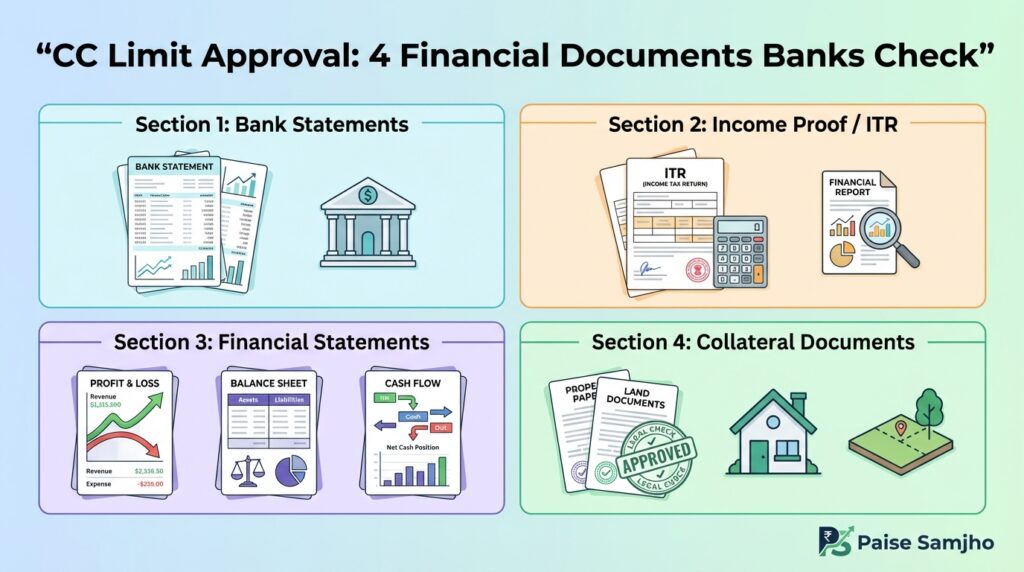

4. Bank Statements

जब आप CC Limit के लिए आवेदन करते हैं, तो बैंक आपके bank statements को ध्यान से जांचता है। इससे बैंक को यह समझने में मदद मिलती है कि आपके business में कितने transactions होते हैं, cash flow कैसा है और business की financial stability कैसी है

Bank statement से यह भी पता चलता है कि आपका business account नियमित रूप से active है या नहीं और उसमें monthly inflow और outflow कितना होता है। अगर आपके account में नियमित और healthy transactions होते हैं, तो CC Limit approval की संभावना बढ़ जाती है।

Usually Required: पिछले 6 से 12 महीनों का bank statement

कई banks यह भी देखते हैं कि आपके account में bounced payments, overdrafts या irregular transactions तो नहीं हैं। इसलिए CC Limit के लिए apply करने से पहले bank account में consistent transactions बनाए रखना जरूरी होता है।

5. Income Proof / ITR

Bank किसी भी loan या credit facility को approve करने से पहले borrower की repayment capacity का आकलन करता है। इसके लिए bank आपसे income proof और Income Tax Return (ITR) मांग सकता है। ITR documents से bank को यह पता चलता है कि आपकी annual income कितनी है, business profit कितना है और आपकी tax compliance कैसी है।

अगर आपका business नियमित रूप से income generate कर रहा है और आपने समय पर ITR file किया है, तो bank के लिए आपकी financial credibility मजबूत मानी जाती है।

Required Documents:

- पिछले 2–3 सालों के Income Tax Return (ITR)

- Income Computation Statement

इन documents की मदद से bank यह evaluate करता है कि applicant CC Limit से लिया गया पैसा समय पर repay करने में सक्षम है या नहीं।

6. Financial Statements

Business applicants को कई बार अपने financial statements भी submit करने पड़ते हैं। इन documents से bank को business की overall financial performance और profitability के बारे में जानकारी मिलती है। Financial statements के माध्यम से bank यह समझता है कि business profit में चल रहा है या loss में, उसके assets और liabilities क्या हैं, और cash flow कितना stable है।

Common Financial Statements:

- Profit & Loss Statement: यह document business की income और expenses का पूरा विवरण देता है। इससे यह पता चलता है कि business कितना profit कमा रहा है।

- Balance Sheet: Balance sheet में business के assets, liabilities और owner’s equity की जानकारी होती है, जिससे business की financial position समझ में आती है।

- Cash Flow Statement: यह statement business में आने और जाने वाले cash का record दिखाता है। इससे bank यह analyze करता है कि business में cash flow stable है या नहीं।

ये financial documents bank को business की financial strength और sustainability समझने में मदद करते हैं।

7. Collateral Documents (अगर Secured CC Limit हो)

कई banks secured CC Limit प्रदान करते हैं, जिसमें borrower को loan के बदले collateral security देनी होती है। Collateral आमतौर पर property, land या किसी valuable asset के रूप में होता है। Collateral देने का उद्देश्य यह होता है कि अगर borrower future में repayment करने में असमर्थ हो जाता है, तो bank के पास security के रूप में asset मौजूद रहे।

Collateral Documents Examples:

- Property Documents: अगर property collateral के रूप में दी जा रही है, तो उसकी ownership और legal papers जमा करने होते हैं।

- Land Papers: अगर land security के रूप में दी जाती है, तो उसके ownership documents और land records आवश्यक होते हैं।

- Property Valuation Report: Bank property की market value जानने के लिए valuation report मांग सकता है, जिससे loan limit तय करने में मदद मिलती है।

- NOC / Legal Clearance: कई मामलों में property पर किसी प्रकार का legal dispute न हो, इसके लिए legal clearance या NOC भी जरूरी हो सकता है।

Collateral documents के आधार पर bank borrower को higher CC limit और बेहतर approval chances दे सकता है।

Cash Credit (CC) Limit क्या होती है? Features, Requirement और Complete Guide

CC Limit Approval के लिए Smart Tips

Cash Credit (CC) Limit approval पूरी तरह आपके business की financial stability और credibility पर निर्भर करता है। अगर आप कुछ smart financial practices follow करते हैं, तो CC limit approval के chances काफी बढ़ सकते हैं। नीचे कुछ important tips दिए गए हैं जो CC limit approval में आपकी मदद कर सकते हैं।

1. अच्छा Credit Score Maintain करें

Bank CC limit approve करने से पहले applicant का credit score (CIBIL score) जरूर check करता है। अगर आपका credit score 750 या उससे ज्यादा है, तो approval मिलने की संभावना ज्यादा होती है।

Credit score अच्छा रखने के लिए:

- Existing loans और credit cards की EMI समय पर pay करें

- Loan default से बचें

- Credit utilization limit कम रखें

2. Business Financials Strong रखें

Bank हमेशा ऐसे businesses को preference देता है जिनकी financial performance stable और profitable हो।

इसलिए जरूरी है कि आप:

- Regular profit दिखाएं

- Proper financial statements maintain करें

- Business में healthy cash flow रखें

Strong financial records bank को confidence देते हैं कि borrower repayment करने में सक्षम है।

3. Proper Documentation रखें

Incomplete या गलत documents होने से CC limit application delay या reject हो सकती है। Apply करने से पहले सभी जरूरी documents तैयार रखें, जैसे:

- Identity Proof

- Business Registration Documents

- Bank Statements

- ITR / Income Proof

- Financial Statements

Complete documentation से approval process तेज और आसान हो जाती है।

4. Business Turnover Improve करें

Banks अक्सर CC limit decide करते समय business turnover को भी ध्यान में रखते हैं अगर आपका business:

- Consistent sales कर रहा है

- Regular transactions हो रहे हैं

- Revenue stable है

तो bank higher CC limit approve कर सकता है।

5. Collateral Offer करने पर विचार करें

अगर आप secured CC limit के लिए collateral security देते हैं, तो approval chances काफी बढ़ सकते हैं। Collateral के रूप में आप:

- Property

- Lan

- Commercial assets

जैसी valuable assets offer कर सकते हैं। Collateral होने से bank का risk कम हो जाता है, इसलिए loan approval आसान हो सकता है।

6. Bank के साथ अच्छा Relationship बनाएं

अगर आपका business account उसी bank में है जहां आप CC limit के लिए apply कर रहे हैं, तो approval आसान हो सकता है। Regular banking relationship जैसे:

- Active current account

- Regular deposits और withdrawals

- Clean transaction history

bank को applicant की reliability समझने में मदद करते हैं।

निष्कर्ष (Conclusion)

Cash Credit (CC) Limit businesses के लिए एक useful facility है जो working capital जरूरतों को पूरा करने में मदद करती है। सही documents, good credit score और strong financial records होने से CC limit approval के chances बढ़ जाते हैं। इसलिए apply करने से पहले अपनी financials और documentation properly prepare करना जरूरी है।

यह article केवल informational purpose के लिए है। CC limit की eligibility, interest rate और document requirements हर bank में अलग हो सकती हैं। Apply करने से पहले संबंधित bank से latest information जरूर check करें।

ऐसी ही simple और useful finance information के लिए Paise Samjho को follow करें और हमारी website पर banking, loans और business finance से जुड़ी और guides पढ़ें। 🚀